By: Charles_Carnevale

Investing Diversification: Is It All It's Cracked Up To Be? There's an old clich? about real estate investing that states that the three cardinal rules are: location- location- location. Clever pundits have borrowed upon this refrain and glibly state that the three most important or cardinal rules of investing are: diversify- diversify- diversify. However, careful analysis will reveal that diversification is a multifaceted concept that has different meanings, benefits and even risks depending on how it's used and what its ultimate purpose is. Therefore, my goal is to examine this ubiquitous investing concept from various angles and perspectives.

There's an old clich? about real estate investing that states that the three cardinal rules are: location- location- location. Clever pundits have borrowed upon this refrain and glibly state that the three most important or cardinal rules of investing are: diversify- diversify- diversify. However, careful analysis will reveal that diversification is a multifaceted concept that has different meanings, benefits and even risks depending on how it's used and what its ultimate purpose is. Therefore, my goal is to examine this ubiquitous investing concept from various angles and perspectives.

Diversification Within or Across

When thinking about diversification there are at least two broad categories to contemplate. The first I would call broad diversification or spreading the risk across numerous asset classes. To me, this is analogous to the throw as much mud on the wall as you can while hoping that some will stick idea. Many experts advocate the diversifying broadly approach. However, to my way of thinking, the idea of diversifying just for diversification sake is not always a sound idea. In other words, I would never advocate putting money into an investment that prudent analysis indicated was a bad place to invest just for the sake of so-called diversification.

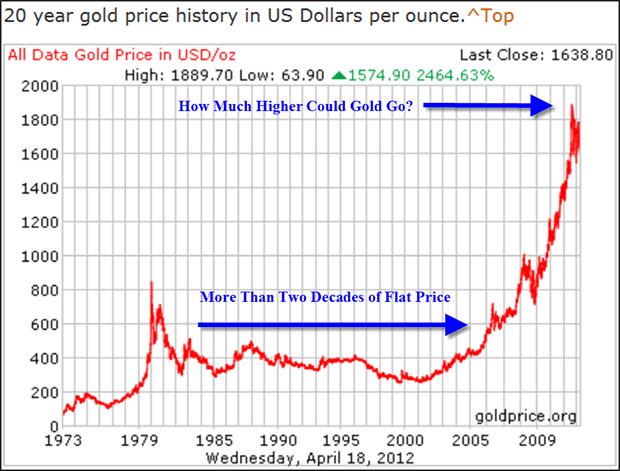

For example, and I know it is going to generate strong disagreement, I think gold is an asset class at a bubble valuation that should be currently avoided. Personally, I sold mine last summer. The following graph courtesy of Goldprice.org says it all. Gold was an attractive investment in the late 1990's to early 2000's, but it is clearly at extremely high levels now. Therefore, I would suggest taking some (or even all) profits. As I have written before, I feel that fixed income (bonds, etc.) is also at an extreme, and therefore, I temporarily also favor avoiding this asset class. I feel that asset classes should only be used for diversification when they are prudent and sound. To force money into a dangerous investment solely for an artificial commitment to diversification makes no sense to me.

Gold a Twenty year History (Courtesy of Goldprice.org)

Furthermore, I tend to have a much narrower view of asset classes than many of my peers. Regarding liquid assets I see only what I call owner-ship or loaner-ship. Where owner-ship represents equity with the investor positioning themselves as an owner/shareholder, and loaner-ship where the investor loans their money at interest. Others might call this equity versus fixed income or stocks versus bonds. In addition to these liquid assets there would also be hard assets such as real estate, precious metals, commodities and art forms that could be considered as options. But the most important point is that deciding what the most appropriate or optimum percentage of your assets should be allocated to these various asset classes is a subject of much debate.

Diversification-what is the goal?

The most common definition, and therefore use, of diversification is as a risk management technique. This most basic concept of diversification says that you should not put all of your eggs in one basket. On the other hand, assuming that this is wise counsel raises the question: how many baskets is the appropriate number? Should you spread your money over 5 baskets, 10 baskets, 20 baskets, 100 baskets or 1000 baskets? In other words, what is the optimum number of baskets; how many baskets are enough and/or how many are too many?

When dealing with broad diversification, I refer you back to my previous comments regarding equity versus debt. There are many who advocate cute little rules that they promote as the proper way to apply broad diversification. For example, one of the more popular rules of thumb goes something like this: Subtract your age from 100 and put the resulting percentage in stocks; the rest in bonds. In other words, if you're 20 years old, put 80% of your assets in stocks; 20% in bonds. If you are 60 years old, put 40% of your assets in stocks and 60% in bonds, etc. Somehow, these little rules of thumb leave me cold. To my way of thinking, a proper asset allocation plan should be based on the individual's goals, objectives and risk tolerances. When dealing with these kinds of issues, one size rarely fits all.

Next there's the issue of whether your diversification objectives are geared towards reducing risk or maximizing return. An investor with a high tolerance for risk would take a different view of what optimum diversification is versus a person who is very risk averse. An individual with a high tolerance for risk might choose only to invest in equities in lieu of owning any fixed income assets. Who can say that this is a bad decision when it suits the investors' goals and risk tolerances? This then takes us to the questions pertaining to optimum diversification within an asset class.

The most interesting aspect of these important questions is the fact that there is no consensus view. Some experts argue in favor of more diversification while others favor less. For example, Charlie Munger, the famed partner of Warren Buffett, believes that 3 to 5 companies in a stock portfolio is enough diversification. Charlie is alleged to have said that diversification is for idiots. And he is quoted as saying: "wide diversification, which necessarily includes investment in mediocre businesses, only guarantees ordinary results. " Alternatively, Warren Buffett seems to agree and has said: "diversification is protection against ignorance."

In contrast, Peter Lynch, the famed manager of the Fidelity Magellan Fund during its glory years held more than 1000 stocks in his portfolio. What is most amazing about this fact is that Peter created one of the strongest long-term track records of any mutual fund that ever existed. Ironically, this is the same man who is credited with coining the phrase "di-worse-i-fication." What many people fail to realize about this is that Peter was referring to an individual company diversifying outside of its core competency through acquisitions. Yet when building his own portfolio, he was happy to own hundreds or even thousands of individual companies.

Then of course there is another aspect of diversifying within an asset class. As it pertains to equities, investors could have a choice of various classes of common stocks. These would include growth stocks versus dividend paying stocks, small stocks versus large stocks, etc. Once again, the investor is faced with the issue of how much should be in growth, how much should be in value, how much should be in large, how much of the small, and on and on. I don't believe there is a general answer. The right answer is the answer that best fits the individual's needs and goals.

And the same concept would apply to investing in bonds. A prudent bond investor might want to ladder their portfolio over various maturities. How much they would allocate to longer maturities versus how much they would allocate to shorter maturities would depend on their belief as to where interest rates might be headed in conjunction with where they feel they are today. If the investor feels that rates are very low they would want to rely more on shorter maturities so that their money would mature into higher interest rates, if they believe rates were going higher. Conversely, if they feel that interest rates are very high they would want to orient their portfolio to the longest maturities possible in order to lock in the higher rates for as long as they possibly could. These considerations would have a major impact on their overall diversification strategy.

There is another argument that the Buffets and Mungers of the world offer against broad diversification. These investors who favor a more concentrated approach believe in essentially two things. First, they believe that extraordinary above-average investments are rare. They further argue that every investment you add would be, or should be, of lesser opportunity than your best choice is. In other words, your best stock will generate a higher return than your second best and so on. Their second belief is that you can only truly know enough about a very select number of companies to be able to invest wisely. Therefore, the more companies you include in your portfolio, the more diluted your knowledge about each will be. In other words they believe in placing all their eggs in one basket (or at least a very few baskets) and then watch that basket very carefully.

Diversification For Maximum Return Or Minimum Risk

As I've previously alluded, diversification is most commonly thought of as a way to reduce risk. However, the opposite side of the diversification coin is rate of return. Diversification, or the lack thereof, will have or should have a large and direct impact on the ultimate return that a portfolio will generate. However, the precise impact is once again a matter of debate. For example, in theory, the more fixed income a portfolio contains the lower the rate of return it would be expected to generate. In his best-selling book Beating the Street, Peter Lynch offered up this 26th Rule of his 25 Golden Rules of Investing (yes, it was his 26th of 25):

"in the long run, a portfolio of well-chosen stocks and/or equity mutual funds will always outperform a portfolio of bonds or a money market account. In the long run, a portfolio of poorly chosen stocks won't outperform the money left under the mattress."

Or you might prefer Peter's principle number two:

"gentlemen who prefer bonds don't know what they are missing."

Perhaps the moral of this story is that diversification has its pluses, but also has its minuses. While it can protect against risk and even smooth out long-term returns; it accomplishes all this at a cost. The seminal question is whether or not you, the individual investor, is willing or even capable of paying the price? Or put another way, how much rate of return are you willing to give up, to buy how much peace of mind? Again, I see this as an individual decision, and perhaps even more importantly, a function of the amount of knowledge you the individual investor possesses and the amount of volatility risk you can endure. Clearly, most of us are not Charlie Munger or Warren Buffett that can afford the luxury of a highly concentrated portfolio. On the other hand, we don't want to be guilty of "di-worse-ification" either. At the end of the day, finding the right balance is as much a personal thing as it is an ironclad principle. At least it is in my way of thinking.

A Fun Look at Diversification Within the Asset Class Equity (stocks)

As I went through the process of researching diversification I came across some interesting results that frankly astounded me. Therefore, I thought it would be fun to share what I discovered. First of all, the primary goal of my research was an attempt to ascertain how much diversification within an asset class was the appropriate amount. Stated more simply, how many stocks were enough to protect the money and how many stocks were too much to dilute or destroy returns. Although I didn't come up with a precise answer that satisfied me, I did discover some fascinating numbers.

Utilizing the F.A.S.T. Graphs research tool I ran 20-year track records on several well-known indices that contained a low of 30 stocks all the way up to 5000 stocks. Before I ran these various records, I assumed that the indicie with the least number of companies would produce the highest rates of return and vice versa.

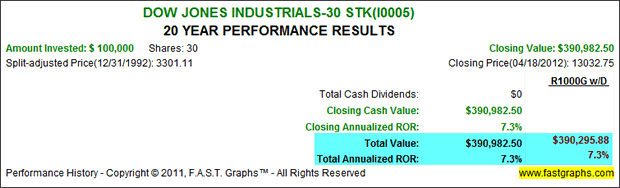

30 Dow Jones Industrials' 20-year Record

My first example is the DJIA, because it is a diversified portfolio but only contains 30 names. As expected, the 30 Dow Jones Industrials did produce the highest rate of return at 7.3% per annum.

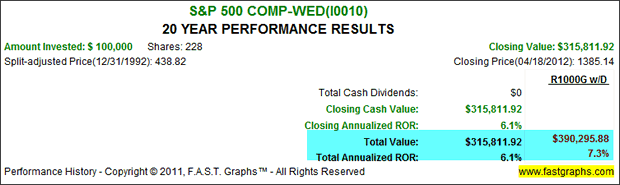

The S&P 500 Without Dividends

My second example is the S&P 500. Since the index contains 500 companies, I expected to see a lower annual rate of return due to the much broader diversification. Even though I was correct, the return differential was only 1.2% per annum coming in at 6.1%. From the standpoint of risk, you could say that you didn't give up much return for the greater safety.

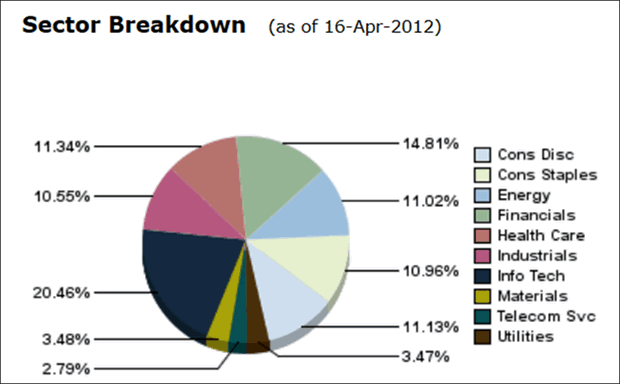

Since this article is all about diversification, I have included the sector breakdown of the S&P 500 in order to illustrate the diversification within this broad index. I found it interesting that Information Technology was the biggest sector at 20.46%. To me this indicates that the S&P 500 is actually an aggressive index, even though it is diversified.

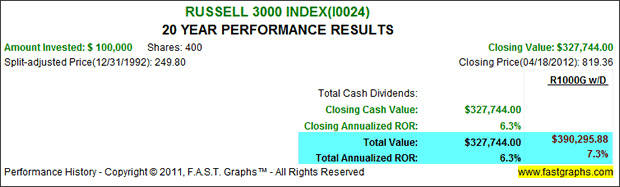

Russell 3000 Index Without Dividends

With my third example I increased the size of the universe by a factor of 5 by calculating the Russell 3000. Astonishingly, this larger universe actually generated a modestly higher rate of return of 6.3% per annum versus 6.1% for the S&P 500. In this case, greater diversification actually increased my return, but not by very much.

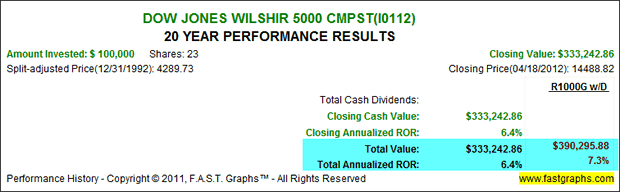

The Dow Jones Wilshire 5000

With my final example I calculated the Dow Jones Wilshire 5000 composite which at 5000 names was the biggest index I could find. Remarkably, this biggest index of all produced the highest rate of return at 6.4% per annum.

Frankly, I'm not really certain what to make of the results I discovered. From what I learned, diversification doesn't really impact the rate of return by very much when looked at from the perspective of the average company in the universe. This led me to wondering what a universe of the top 10 best performing stocks might look like. Of course I recognize that the flaw in this line of thinking would be having the foresight to pick the top 10 at the beginning of this exercise. However, my curiosity was not about being smart enough to pick the very best; instead, I was just curious to know what the differentials would actually be.

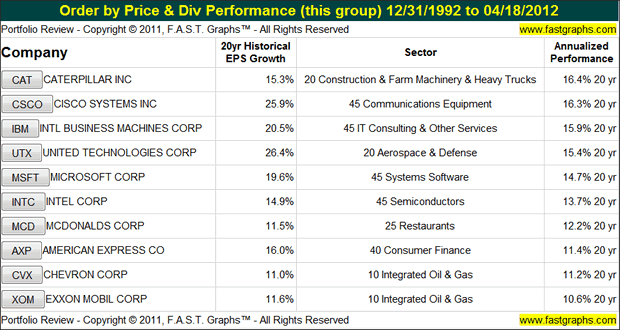

Therefore, I first sorted the top 10 of the 30 Dow Jones Industrials and listed them in order of best-performing to lowest-performing for the past 20 years. The average performance of an equally weighted investment in each of these candidates would have averaged approximately 13.8% per annum which is just shy of doubling the rate of return for the entire composite of 30 names. To put this into perspective, $1 million equally allocated total investment spread into these top 10 companies would grow to over $12 million in 20 years. I thought this was interesting, but not terribly exciting. The following table shows the results of the top 10 best-performing 30 Dow Jones Industrials with $100,000 invested in each at the beginning of 1993.

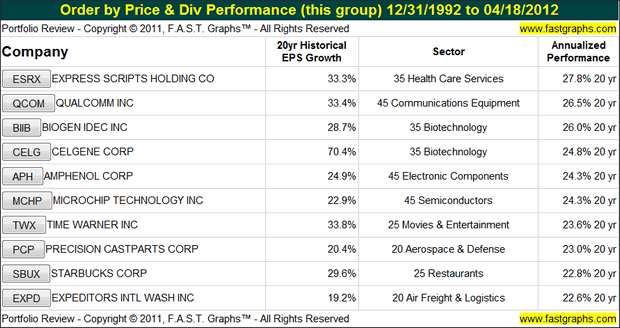

With my second example I went to the larger universe of the S&P 500. With a much bigger universe to draw upon a discovered a significantly higher average rate of return. As it relates to diversification, I'm really not sure what this means other than a bigger universe offered a much bigger opportunity to find significantly above-average investments. The top 10 best-performing S&P 500 companies produced an average return of almost 25% per annum. Therefore, the same $1 million equally allocated across these 10 names grew to over $68 million. Now, that number got my attention.

Now, once again, admitting that this last little exercise is fraught with error, I do feel that it revealed some interesting information. Perhaps most importantly, it did reveal a large disparity between the best performers versus the average performance. If you did possess the skills of a legendary investor, you just might be better served to focus your attention on only a few of the very best companies you could identify. However, for the rest of us we might be best served by placing our money spread out and into more baskets.

Summary and Conclusions

As I began digging into the many faces of diversification, I quickly learned that it is a much more complex concept than at first meets the eye. But perhaps most importantly of all, I feel I learned that there is no one-size-fits-all or even a set of universally applicable rules or principles. To a great extent, diversification turns out to be a very personal issue. How much or how little depends more on your goals and objectives, the knowledge and experience you possess, the time you can allocate to your investment portfolio, and of course, your tolerance for risk. Some of us need a great deal of diversification, while others could do with a lot less.

I will conclude this article by confidently stating that it only scratches the surface of what a comprehensive treatise on diversification would require. In many ways, I feel that I raised more questions than I answered. Therefore, I expect that more articles will be forthcoming. The one area that I feel I shortchanged the most was the area of broad diversification across many different asset classes. Consequently, an article dealing specifically with this aspect of diversification seems like a logical next step. However, I will end by saying once again that I believe that it is also a very personal concept. On the other hand, I do believe that no asset class should ever be used unless it makes prudent economic sense to include it.

Disclosure: Long MCHP, MSFT, CVX, ESRX, XOM, UTX, CSCO & INTC at the time of writing.

By Chuck Carnevale

http://www.fastgraphs.com/

Charles (Chuck) C. Carnevale is the creator of F.A.S.T. Graphs?. Chuck is also co-founder of an investment management firm.? He has been working in the securities industry since 1970: he has been a partner with a private NYSE member firm, the President of a NASD firm, Vice President and Regional Marketing Director for a major AMEX listed company, and an Associate Vice President and Investment Consulting Services Coordinator for a major NYSE member firm.

Prior to forming his own investment firm, he was a partner in a 30-year-old established registered investment advisory in Tampa, Florida. Chuck holds a Bachelor of Science in Economics and Finance from the University of Tampa. Chuck is a sought-after public speaker who is very passionate about spreading the critical message of prudence in money management. Chuck is a Veteran of the Vietnam War and was awarded both the Bronze Star and the Vietnam Honor Medal.

? 2012 Copyright Charles (Chuck) C. Carnevale - All Rights Reserved Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

? 2005-2012 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.

Comments

Post Comment (Moderated)

drew barrymore bill o brien portland trailblazers will kopelman casey anthony leann rimes dakota fanning

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.